Startup Success in 2025: Best 10 Fractional CFO Services to Lower Burn Rate & Grow Profits

Does the idea of hiring an accountant for your business make you overwhelmed? Employing the

We drive profitability and growth for small businesses!

Have you ever thought about how businesses handle their accounts and finances efficiently? How do they organize a myriad of financial transactions and make sense of it all? The answer lies in a powerful tool known as the “Chart of Accounts.” This vital framework forms the backbone of financial management, enabling businesses to structure and categorize their financial activities for clearer insights and informed decision-making.

In this guide, we’ll walk you through the ins and outs of the Chart of Accounts (COA) and provide real-world examples to illustrate its significance. Let’s embark on this journey to unravel the mysteries of financial organization and equip you with the knowledge to optimize your financial systems effectively.

The Chart of Accounts acts as a roadmap, categorizing all financial transactions within an organization. It’s like a filing cabinet with folders for various aspects of a company’s financial operations. Think of it as your financial GPS, guiding you through the labyrinth of revenue, expenses, assets, and liabilities.

Have you ever wondered how a well-structured Chart of Accounts could streamline your financial reporting? Stick with us as we reveal the key elements and benefits of mastering this essential tool.

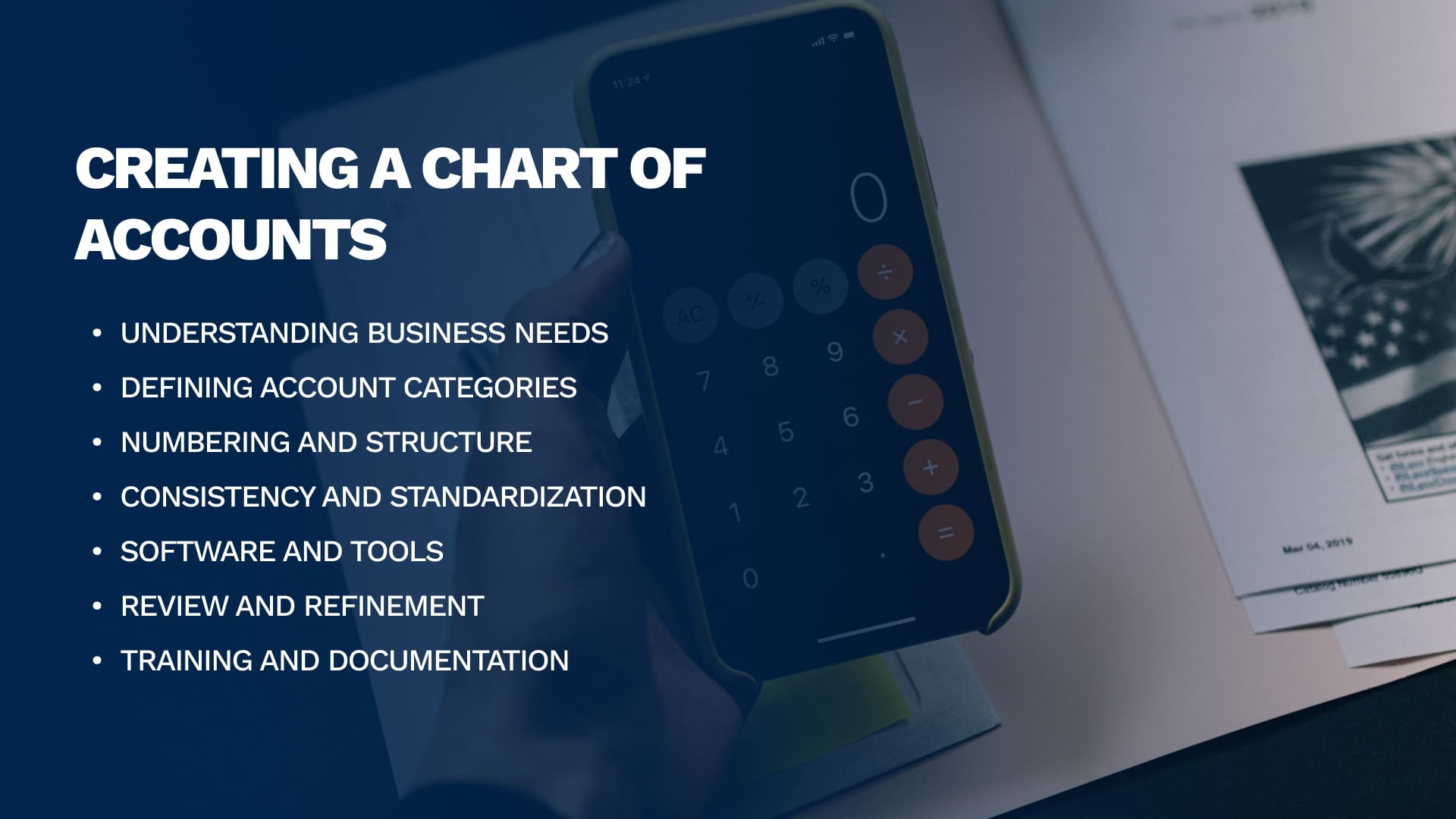

Before diving into creating a Chart of Accounts, it’s crucial to understand the specific needs and nature of your business. Consider the industry, size, complexity, and unique financial reporting requirements. Tailoring the Chart of Accounts to your business’s operations ensures it effectively captures and categorizes all relevant financial transactions.

Start by outlining the main account categories based on standard accounting principles: assets, liabilities, equity, revenue, and expenses. Within these categories, further subdivide accounts to accommodate specific types of transactions relevant to your business. For instance, under assets, create accounts for cash, inventory, equipment, and investments.

Develop a systematic numbering system and structure for accounts to facilitate organization and ease of use. This numbering convention typically follows a hierarchical structure, with each account having a unique code. The structure should allow for scalability and flexibility to accommodate future expansions or changes.

Maintain consistency in naming conventions and account structures throughout the Chart of Accounts. Clear, standardized naming ensures uniformity across accounts, making it easier for users to locate and understand different accounts’ purposes.

Leverage accounting software or specialized tools to create and manage your Chart of Accounts efficiently. Many software options offer predefined templates or customizable frameworks that align with industry standards. Utilizing these tools simplifies the Chart of Accounts creation process and streamlines ongoing management.

Regularly review and refine your COA to ensure it stays relevant and aligned with evolving business needs. As your business grows or diversifies, update the Chart of Accounts to accommodate new accounts or modify existing ones for improved financial reporting accuracy.

Provide adequate training to personnel responsible for using the Chart of Accounts. Document guidelines, procedures, and explanations for each account to ensure consistent understanding and usage across the organization. Effective training enhances accuracy and minimizes errors in recording financial transactions.

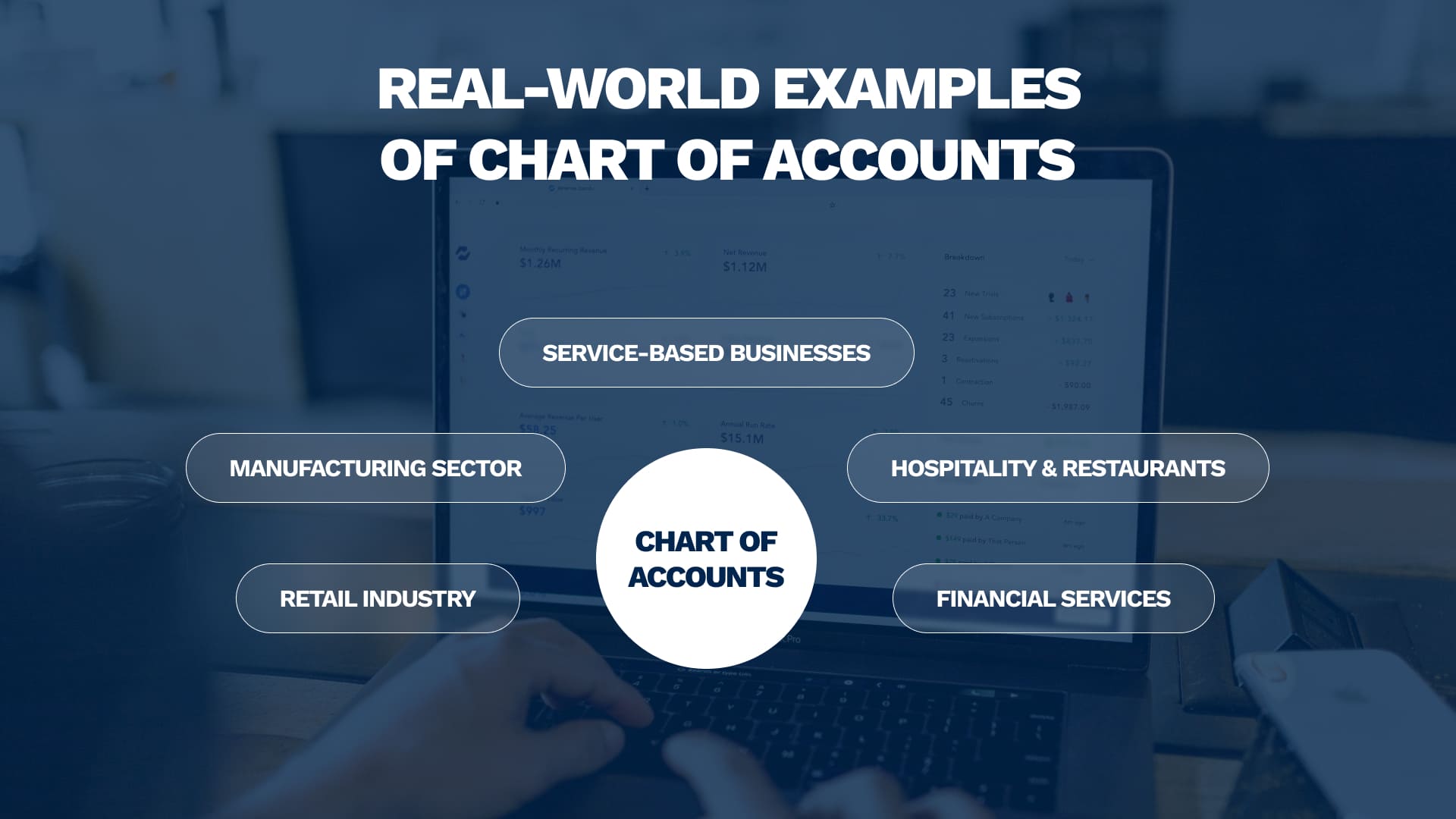

Theory meets reality as we delve into practical examples from diverse industries. See firsthand how businesses across different sectors structure their COAs to suit their unique financial requirements. These case studies will illuminate the versatility and adaptability of the COA in various real-world scenarios.

In retail, COAs often segregate accounts for inventory, sales, cost of goods sold (COGS), and various expense categories. For instance, a retail Chart of Accounts might have detailed sub-accounts for different product lines or departments. It helps track sales revenues, inventory levels, and specific expenses like advertising, rent, or utilities.

In manufacturing, Chart of Accounts tend to be more intricate due to the complexity of operations. They encompass accounts for raw materials, work-in-progress, finished goods, production costs, and overhead expenses. Each phase of production has dedicated accounts, aiding in cost tracking, inventory valuation, and operational analysis.

Service-oriented businesses often have simpler Chart of Accounts focusing on revenue streams and operational expenses. They might include accounts for service revenue, client invoices, professional fees, and operating expenses like salaries, marketing, and office supplies.

Non-profits’ COAs differentiate between various funding sources, donations, program-related expenses, administrative costs, and fundraising efforts. Segregation of accounts is crucial to demonstrate fiscal responsibility to donors and regulatory bodies.

In the hospitality industry, Chart of Accounts can be intricate, encompassing revenue streams like room sales, food and beverage sales, expenses related to staff, supplies, marketing, and utilities. Each department, such as housekeeping, F&B, or administration, might have specific accounts for detailed financial tracking.

For banks, credit unions, or financial service firms, Chart of Accounts are designed to manage diverse financial instruments, loans, deposits, securities, interest income, and operational expenses like salaries, marketing, and compliance costs. These Chart of Accounts comply with stringent regulatory standards for reporting and transparency.

Within the Chart of Accounts, various account types serve distinct purposes. We’ll break down the different categories—assets, liabilities, equity, revenue, and expenses—providing clear definitions and practical examples for each. Understanding these account types is key to effectively organizing your financial data.

Asset accounts consist of tangible and intangible resources owned by a business. These can include cash, accounts receivable, inventory, property, equipment, investments, and intellectual property. Asset accounts are crucial in determining a company’s financial health and its ability to meet short- and long-term obligations.

Liability accounts represent obligations or debts owed by a business to external parties. Examples include accounts payable, loans, accrued expenses, and deferred revenue. Tracking liability accounts is vital for assessing a company’s financial obligations and its ability to settle debts.

Equity accounts reflect the residual interest or ownership in a business after deducting liabilities from assets. Common equity accounts include owner’s equity, retained earnings, and capital contributions. Equity accounts signify the ownership stake and measure a company’s net worth.

Revenue accounts record income generated from a company’s primary operations. Sales revenue, service fees, interest income, and rental income fall under revenue accounts. These accounts demonstrate the financial inflows from core business activities.

Expense accounts represent the costs incurred to generate revenue. They include operational expenses such as salaries, utilities, rent, advertising, supplies, and depreciation. Expense accounts are essential in assessing a company’s cost structure and profitability.

Contra accounts offset or reduce the balance of a related account. Examples include accumulated depreciation (offsetting the asset’s value) or allowance for doubtful accounts (offsetting accounts receivable). Contra accounts are used to provide a more accurate representation of the related accounts.

Interim accounts, also known as temporary accounts, track financial activities for a specific accounting period. Revenue and expense accounts fall into this category. These accounts are closed at the end of the accounting period to prepare for the next reporting cycle.

Maintain uniformity in naming accounts throughout the COA. Clear, descriptive, and standardized names make it easier for users to identify and understand each account’s purpose. Consistency in naming conventions streamlines financial reporting and ensures clarity across the organization.

Organize accounts in a logical and intuitive manner. Establish a hierarchical structure that aligns with the business’s operations and reporting requirements. Group similar accounts together under relevant categories for easy navigation and comprehension.

Implement controls that separate the responsibilities of creating, managing, and accessing the COA. This segregation of duties helps prevent errors, unauthorized changes, and ensures accountability in maintaining the integrity of the COA.

Document clear guidelines, explanations, and definitions for each account within the COA. This documentation aids in training new personnel, minimizes confusion, and ensures consistent understanding and usage of accounts across the organization.

Conduct periodic reviews and updates of the COA to keep it aligned with evolving business needs. As the business expands, changes in operations or regulatory requirements may necessitate additions, modifications, or deletions of accounts. Regular updates ensure the COA remains relevant and accurate.

Design the COA structure to accommodate potential future changes or expansions. Incorporate flexibility into the numbering system or account structure to easily add new accounts or modify existing ones without disrupting the entire framework.

Provide comprehensive training to personnel involved in utilizing the COA. Ensure that users understand the COA’s structure, purpose, and how to correctly categorize transactions. Ongoing education about updates or changes to the COA is essential for maintaining accuracy.

Ensure compliance with accounting standards and regulations when designing and managing the COA. Adhering to industry-accepted standards enhances credibility, accuracy, and consistency in financial reporting.

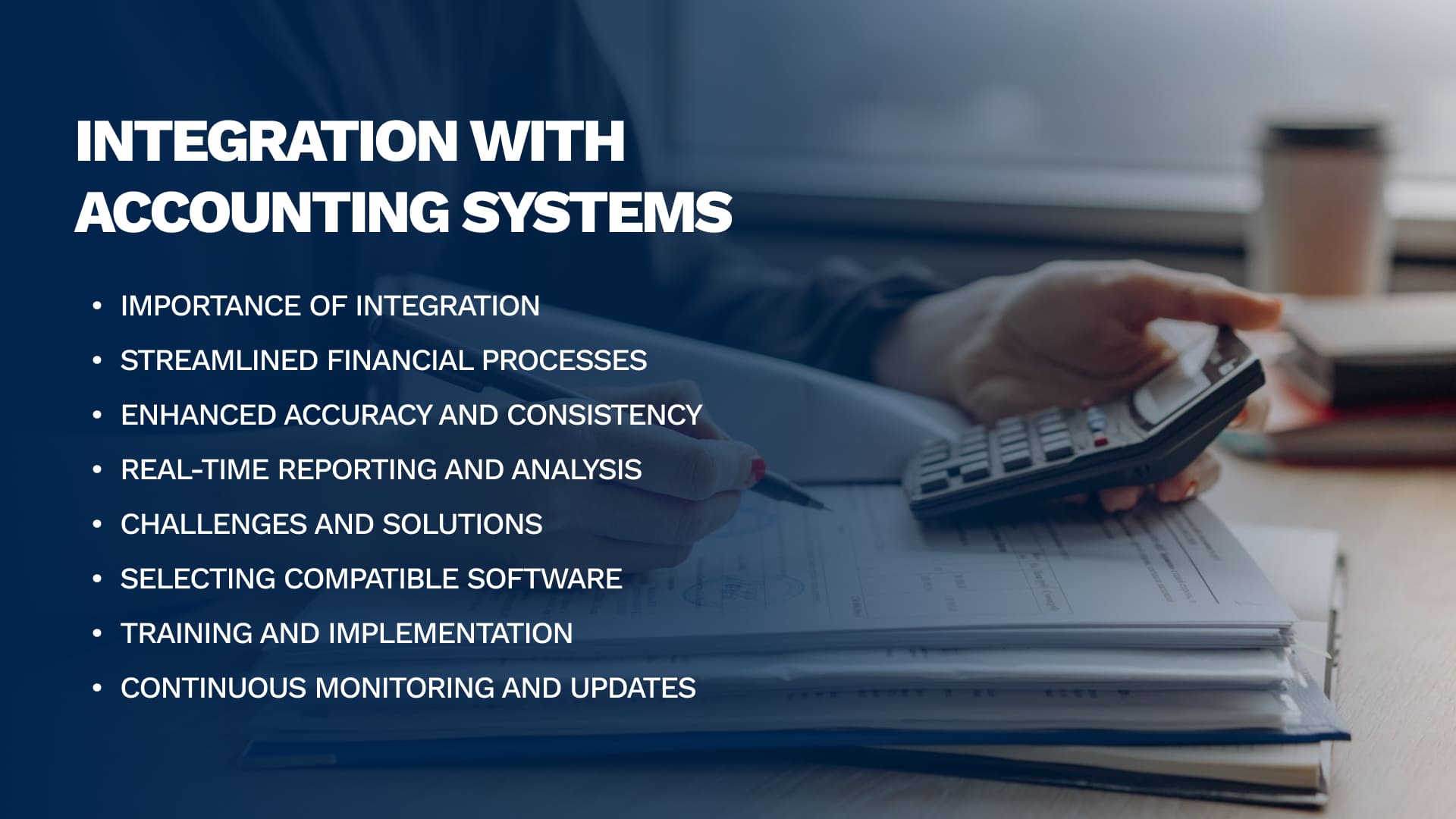

Integrating the COA with accounting software or systems streamlines financial operations by automating data entry, ensuring accuracy, and facilitating real-time reporting. It enables a direct link between financial transactions and the COA, reducing manual errors and enhancing efficiency.

Integration allows for a smooth flow of information between different modules or components of an accounting system. When a transaction occurs, it automatically reflects in the corresponding COA account, eliminating the need for manual input and reducing the risk of discrepancies.

Automated integration ensures consistency and accuracy in recording financial data across the COA and the accounting system. It minimizes the chances of human error and ensures that all transactions are accurately categorized within the COA’s framework.

Integration enables real-time access to financial data, empowering businesses to generate up-to-date reports and conduct immediate analysis. This timely access to information aids in informed decision-making and allows for quick adjustments based on current financial insights.

While integration offers numerous benefits, challenges may arise, such as compatibility issues between different software or data synchronization errors. Addressing these challenges requires selecting compatible software, proper configuration, and regular system checks to ensure seamless integration.

When choosing accounting software, ensure compatibility with your existing COA structure. Opt for systems that allow easy mapping of COA accounts and provide customizable options to align with specific business needs.

Comprehensive training for staff on using integrated systems is crucial. Adequate training ensures that employees understand how to navigate the integrated software, correctly input data, and utilize the COA effectively within the system.

Regular monitoring of the integrated system is essential to identify and address any discrepancies or errors promptly. Additionally, updates and upgrades to both the COA and the accounting software must be synchronized to maintain integration effectiveness.

The Chart of Accounts serves as the cornerstone of efficient financial management, offering clarity and structure in the ever-evolving world of business finance. By mastering its intricacies and implementing best practices, you empower your business to make informed decisions and navigate financial complexities with confidence.

At Profit Spear, our mission is to empower your financial journey. We handle your finances with the utmost integrity, ensuring accurate bookkeeping, transparent reporting, and insightful financial statements. Let us equip you with the tools needed for smart financial decisions, reduced taxes, and smooth accounting services—propelling your business toward success.

Does the idea of hiring an accountant for your business make you overwhelmed? Employing the

Does the idea of hiring an accountant for your business make you overwhelmed? Employing the

Does the idea of hiring an accountant for your business make you overwhelmed? Employing the

Does the idea of hiring an accountant for your business make you overwhelmed? Employing the

Does the idea of hiring an accountant for your business make you overwhelmed? Employing the